Lending Highlights

2024

1988-2024

Number of Loans Closed

100

Number of Loans Closed

2,369

Number of Loans Closed

Dollar of Loans Closed

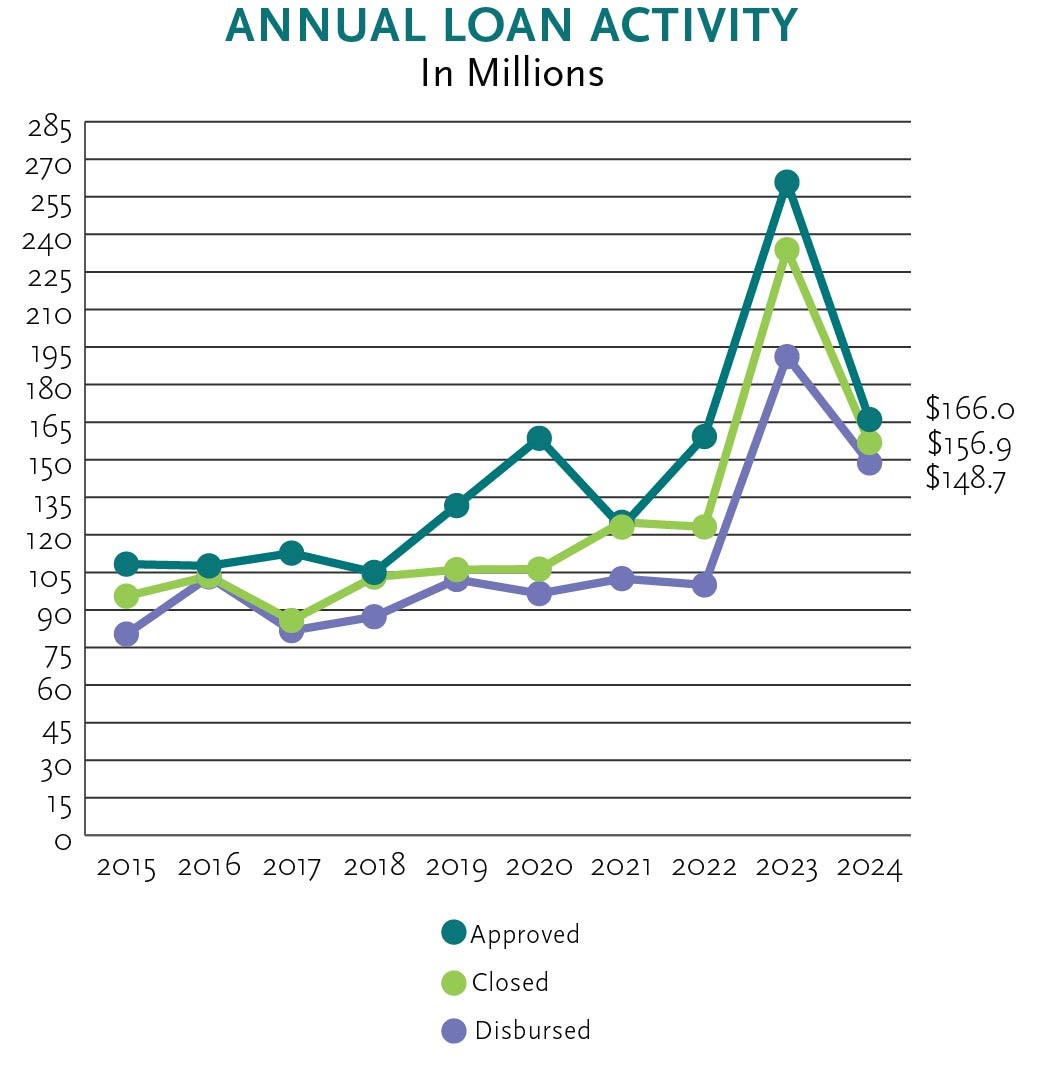

$156.9 million

Dollar of Loans Closed

$1.8 billion

Dollar of Loans Closed

Capital Leveraged

$640 million

Capital Leveraged

$6.7 billion

Capital Leveraged

Number of Nonprofits Served

87

Number of Nonprofits Served

1,282

Number of Nonprofits Served

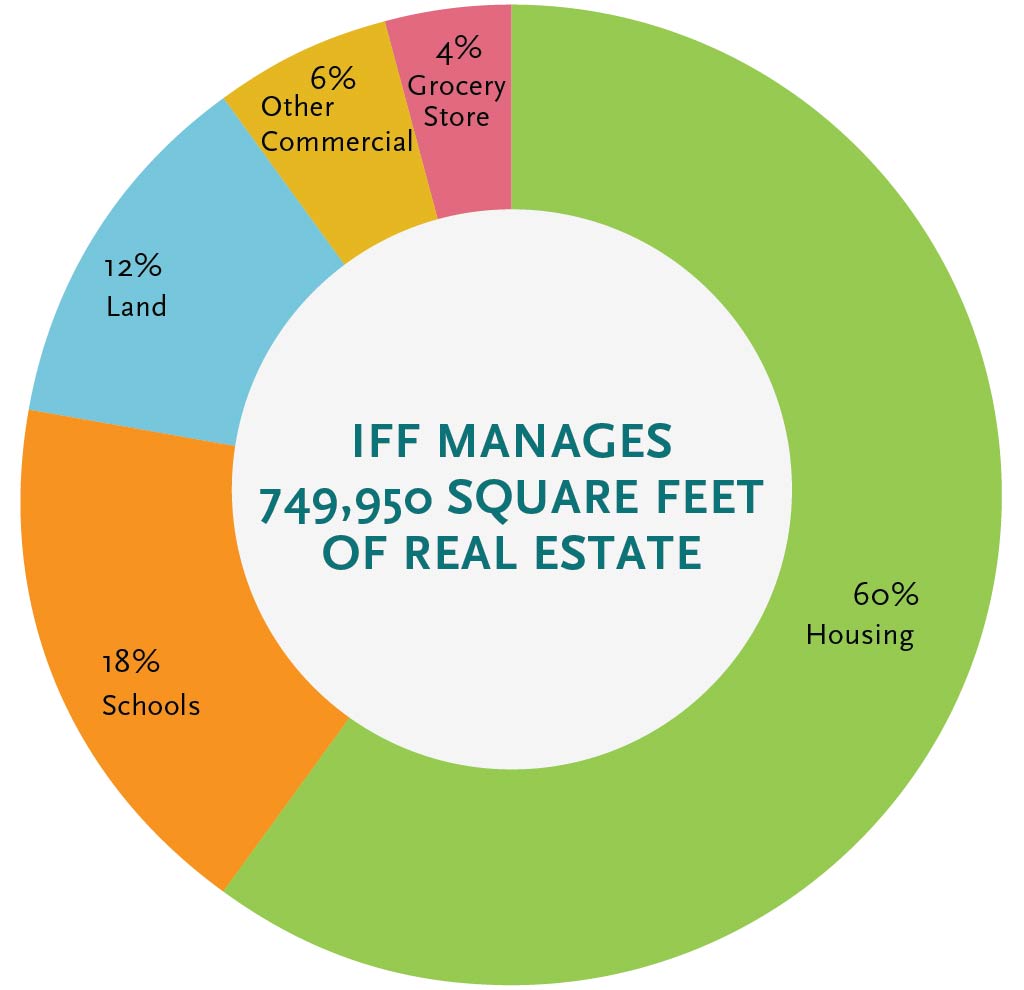

Square Feet of Real Estate Developed by Financing

2.5 million

Square Feet of Real Estate Developed by Financing

43.7 million

Square Feet of Real Estate Developed by Financing